Tax Advantages of Syndications

Disclaimer: I am not a tax expert. The following content is meant for educational purposes only. Please consult with your accountant or lawyer.

1. 🏗️ Depreciation: Paper Losses That Shield Real Income

When you invest in a multifamily syndication, you're investing in a physical asset—a building that naturally depreciates over time. The IRS allows you to deduct a portion of the property's value each year to account for this wear and tear, even though the property may actually be appreciating in market value.

Here’s where it gets even better: through a process called cost segregation, we can accelerate that depreciation. This means breaking down the building into individual components (like plumbing, flooring, and appliances) and depreciating them over shorter timeframes—5, 7, or 15 years instead of the standard 27.5 years.

The result? In the early years of ownership, you’re often able to deduct tens of thousands of dollars in depreciation losses, significantly reducing the taxable income passed through to you as an investor—even if the property is producing strong positive cash flow.

2. 🧾 Pass-Through Losses: Reducing Your Taxable Income

As a passive investor in a syndication, you receive a share of the property’s financials, including income and expenses. Due to depreciation and other deductions, it’s common for these investments to show a “paper loss” on your K-1 tax form, despite the fact that you're receiving cash distributions.

These losses can offset passive income from other investments (such as rental properties or limited partnerships), helping you reduce your overall tax liability. In some cases, if you're classified as a Real Estate Professional or meet other material participation rules, these losses could even offset active income, like W-2 or 1099 earnings. That’s a potential game-changer for high-income professionals.

Even if you’re not a real estate professional, the ability to stack passive losses against passive income makes multifamily syndications a smart way to create tax-efficient income streams.

3. 🔁 1031 Exchange: Deferring Taxes While Growing Wealth

When a syndicated property is sold, investors typically receive a return of capital plus profits. In a traditional sale, those profits would be subject to capital gains taxes and possibly depreciation recapture. However, with a 1031 exchange, it’s possible to defer those taxes by reinvesting the proceeds into another “like-kind” property.

This is one of the most powerful tools available in the tax code for compounding real estate wealth. By rolling profits forward tax-deferred, you preserve more capital to invest and grow. Over time, this can mean significantly higher total returns and more wealth left to your heirs.

At Cardia Real Estate Investments, we aim to structure our exit strategies with the option of 1031 exchanges in mind, so our investors have flexibility when it's time to harvest gains.

4. 📉 Long-Term Capital Gains: Preferential Tax Treatment

Multifamily investments are typically held for more than a year, which means when a property is sold, any profits distributed to you are taxed at long-term capital gains rates. These rates—currently 0%, 15%, or 20% depending on your income—are far lower than the top ordinary income tax bracket of 37% that many physicians fall into.

This shift in taxation category is no small thing. Over time, the savings from paying 15–20% instead of 37% can have a massive compounding effect on your overall net worth.

While your day job may pay well, it’s typically taxed at the highest rates. Real estate, when structured wisely, gives you an avenue to grow wealth more tax-efficiently.

5. 🚫 No Self-Employment or Payroll Taxes on Passive Income

As physicians or business owners, we’re often hit with self-employment taxes or additional payroll taxes like Medicare surtax on earned income. The good news? Income from real estate syndications is classified as passive, which means it’s not subject to these additional taxes.

You don’t pay Social Security or Medicare taxes on the distributions you receive, and you avoid the 15.3% self-employment tax altogether. This creates another layer of tax efficiency that helps your passive income go further—and stay in your pocket.

Below is an example of a 1031 exchange. We are choosing to focus on this since most people are not too familiar with it.

🔁 Example: 1031 Exchange from One Syndication to Another

🏢 Original Investment:

Investor: Sarah, a passive investor in a Cardia Real Estate Investment Syndication

Initial Investment: $100,000 into a 200-unit multifamily deal in Atlanta, GA

Hold Period: 5 years

Total Return: 2× equity multiple (Sarah receives $200,000 at sale: her original $100K + $100K gain)

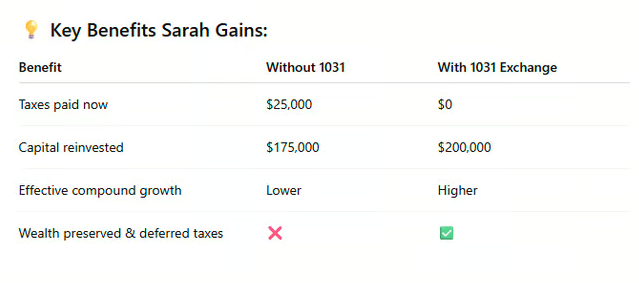

📈 Without a 1031 Exchange:

Capital Gains Tax (assume 20% federal + 5% state):

Sarah pays taxes on the $100K gain → $25,000 in taxesReinvested Capital: $175,000

Her investment base shrinks, and she pays taxes sooner.

🔄 With a 1031 Exchange:

The syndication sponsor (Cardia REI) structures the exit as a 1031-compliant sale.

Sarah elects to roll her $200,000 proceeds into a new 150-unit multifamily project in Monroe, GA.

No capital gains taxes are due at the time of the exchange.

Full $200,000 goes to work in the new deal.

📝 Important Notes:

The 1031 exchange must be properly structured and declared in advance of the original sale.

Investors must identify a replacement property within 45 days and close within 180 days.

Not all syndications support 1031 exchanges. At Cardia Real Estate Investments, we explore 1031-eligible structures where feasible and clearly communicate them to investors in advance.