Tax Updates from the One Big Beautiful Bill

Our guest writer for this issue is Daniel Alvarado, CPA from Tillett, Alvarado, Prendergast & Suarez, Certified Public Accountants. As always, this is for education purposes only. Please consult with your own tax advisor to see what applies to your specific circumstance.

Tel: 561-504-6324

Fax: 561-907-4965

Email: daniel@miketillettcpa.com

Palm Beach Gardens Office

3309 Northlake Boulevard, Suite 203

Palm Beach Gardens, FL 33403

Boca Raton Office (by appointment only)

2799 NW Boca Raton Blvd., Suite H-205

Boca Raton, FL 33431

Daniel is currently an associate professor of taxation at Florida Atlantic University. How he finds time for these activities despite having 5 children is beyond me - but we are grateful for his contribution. If you have any questions, feel free to contact him directly. I personally have used him for several years.

OB3 Real Estate Impact

With the passage of Public Law 119-21 (publicly referred to as “The One Big Beautiful Bill Act” or OB3 for short), many changes will be impacting both personal and business tax preparation starting in 2025. Many of these changes will also have an impact on real estate activities. It is important to be aware of these changes in order to plan accordingly to receive the most benefits from these changes.

State and Local Tax (SALT) Deduction increase

Throughout the creation process of OB3, one big discussion point has been the itemized deductions allowed for state and local taxes that were previously limited to only $10,000 allowed as part of one’s itemized deductions (with the exception of those filing as married filing separately where only $5,000 was allowed). With the passage of OB3, this deduction has increased from a maximum of $10,000 to $40,000 ($20,000 for married filing separately) in 2025 with the maximum deduction increasing for inflation for each following year until 2030 where the deduction amount will revert back to $10,000. The states that do not have state income taxes due such as Florida, Texas, and Washington as some examples, real estate taxes have been one of the largest ways that residents of these states can benefit from this deduction. With the deduction increasing by 400% in 2025, it is now more important than ever to report one’s real estate taxes to receive the full benefit as those with $40,000 in SALT will already be qualified to itemize their deductions instead of using the standard deduction before other considerations such as deductible mortgage interest and charitable donations. It should also be noted though that the amount of allowed deduction starts to be reduced for those who income exceeds $500,000 where the amount of the allowed deduction will be reduced by 30% for every dollar exceeding $500,000 in modified adjusted gross income (MAGI).

Elimination of the Green Tax Credits

One major impact OB3 will have on homeowners is the removal of the energy efficient home improvement credit that has allowed tax credits for the installment of qualified property onto one’s primary residence. Examples of property that can be made for these credits include the installation of a new central A/C unit, heat pumps, and impact windows and doors to name a few. These credits will disappear after December 31, 2025 allowing for only a few months to have these properties installed and placed into service to receive the full benefits of these credits.

Bonus Depreciation

With the passage of the Tax Cuts and Jobs Act (TCJA) of 2017, 100% bonus depreciation was allowed from 2017 to 2022 where qualified property was allowed to be fully depreciated immediately instead of over the life of the property. Starting in 2023, the 100% bonus depreciation was starting to be phased out where each year it would be reduced by 20% (80% depreciation in 2023, 60% depreciation in 2024, 40% depreciation in 2025, etc.) until there was no more bonus depreciation in 2027. The impact of this phase out in bonus depreciation can be seen in the cost seg studies of rental properties. Newer properties that had these studies done on them would not be able to receive the same amount of expenses compared to similar properties that would have these studies done on them prior to 2023 where the total amounts classified as 5-Year and 15-Year properties were allowed to be expensed immediately instead of only a percentage being allowed.

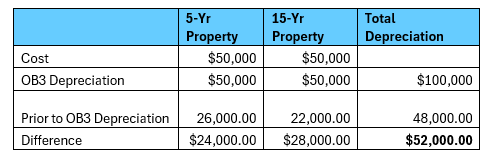

OB3 has allowed for bonus depreciation to be 100% again for properties purchased and placed into service after January 19, 2025. The following example compares the impact this return to 100% bonus depreciation will have compared to if the prior bonus depreciation rules were in place where you can only take bonus depreciation of 40% for 2025 for a cost seg where it was determined that property classified as having a 5-Year useful life were worth $50,000 and property classified as having a 15-Year useful life were worth $50,000:

The above chart shows that the return to 100% bonus depreciation can allow for significantly more deductions to be taken to where even the difference between the allowed depreciation is more than what you would be able to take prior.

Qualified Production Property

A new provision has been created with OB3 that allows for 100% special depreciation for qualified production property that has been put into service after July 4, 2025. This provision applies only to nonresidential property that meet the following requirements:

1. The property is an integral part of a business’s qualified production activity (defined as the manufacturing, production, or refining of a qualified product)

2. The property is placed into service within the United States prior to January 1, 2031

3. You are the original user of the property

4. Construction of the property starts after January 19, 2025 and prior to January 1, 2029 and

5. An election is made for the property to be treated as qualified production property.

This property does not qualified if used for the following activities:

1. Office space

2. Administrative services

3. Lodging

4. Parking

5. Sales Activity

6. Software Development

7. Engineering activities

8. Any other functions that are unrelated to manufacturing production or refinement of tangible personal property.

Conclusion

With the various changes that are coming in 2025 with the passage of Public Law 119-21, it is important to be aware of what specific provisions will impact you directly and what provisions can be an opportunity for tax savings. With a few months still remaining in 2025, there is still sufficient time to consult with a tax professional to devise strategies and plan to maximize your tax savings before the year ends. As shown by the increase in the SALT deduction and bonus depreciation, significant deductions are present now that were not in previous years that can results in thousands of dollars in tax savings with the assistance of proper planning.

Make sure to sign up for our newsletter to receive continuing education right to your inbox.